Every payment you make leaves a trace. For those prioritizing privacy, here are the 7 best anonymous payment methods in 2026:

- Cryptocurrency: Pseudonymous with privacy-focused coins like Monero or Zcash offering enhanced anonymity. Requires wallet setup and is ideal for tech-savvy users.

- Paysafecard: Prepaid vouchers bought with cash for online payments. Fully anonymous when purchased offline.

- Cash App: Uses a $Cashtag for semi-anonymous peer-to-peer transfers but requires account setup.

- Virtual and Masked Credit Cards: Protect real card details with temporary numbers. Great for online shopping but linked to your financial account.

- Prepaid Gift Cards: Buy with cash for anonymity. Best for specific retailers or online purchases.

- Prepaid Debit Cards: Load with cash for broad acceptance without linking to a bank account.

- Cash and Cash-by-Mail: The most private for in-person transactions or online purchases (via mail), though cash-by-mail carries risks.

Quick Comparison:

| Payment Method | Privacy Level | Best For | Key Limitation |

|---|---|---|---|

| Cryptocurrency | High (with care) | Tech-savvy international transfers | Limited merchant acceptance |

| Paysafecard | Full (if offline) | Anonymous online shopping | Limited use in physical stores |

| Cash App | Semi-anonymous | Peer-to-peer transfers | Requires personal details to set up |

| Virtual Credit Cards | Semi-anonymous | Protecting card details online | Limited to linked financial accounts |

| Prepaid Gift Cards | Full (if offline) | Specific retailer purchases | Retailer-specific usage |

| Prepaid Debit Cards | Partial | General purchases | Fees and spending limits |

| Cash and Cash-by-Mail | Full | In-person or mail transactions | Limited online use, mail risks |

Each method balances privacy, convenience, and usability. Choose based on your needs – cryptocurrency and Paysafecard for digital anonymity, prepaid cards for versatility, and cash for unmatched privacy.

Top 5 Anonymous Payment Methods in 2026: Protect your Privacy Online

1. Cryptocurrency

Cryptocurrency offers a distinct way of handling transactions, where payments are tied to a wallet address rather than personal information. Unlike traditional systems that rely on banks or payment processors, cryptocurrencies like Bitcoin function on decentralized blockchain networks. Let’s dive into the key aspects that define cryptocurrency, especially when it comes to privacy, usability, and accessibility.

Privacy Level: Full Anonymity vs. Semi-Anonymous

Most cryptocurrencies are pseudonymous, meaning transactions are associated with wallet addresses rather than real names. However, if a wallet is linked to a verified identity – like through a regulated exchange – this pseudonymity can be compromised. For those seeking greater privacy, options like Monero and Zcash stand out. These privacy-focused coins, along with tools like Wasabi and Sparrow wallets, use features such as coin mixing to obscure transaction details. Mobile wallets like Zashi (tailored for Zcash) also come equipped with built-in privacy features, offering additional layers of protection for your financial data. While privacy is a significant advantage, balancing it with usability and security is critical.

Ease of Use and Accessibility

Using cryptocurrency involves a few technical steps, such as setting up a digital wallet, managing private keys, and purchasing coins – often through exchanges that require identity verification. Thankfully, user-friendly mobile apps have made this process easier, though there’s still a learning curve. One thing to keep in mind: cryptocurrency transactions are irreversible, so securely managing private keys is essential. Transaction speeds vary; Bitcoin confirmations typically take 10–30 minutes, while other cryptocurrencies may process faster. Fees also fluctuate depending on network traffic, sometimes reaching several dollars during busy periods.

Merchant Acceptance and Use Cases

Cryptocurrency adoption among merchants remains limited. It’s most commonly used for online, international, or peer-to-peer transactions rather than for everyday purchases. For many, the appeal lies in the privacy and control it offers over personal financial information, even if it’s not the most convenient payment method.

Geographic Availability

Cryptocurrencies are available worldwide, but local regulations can impact how they’re used. For example, in the United States, anti-money laundering (AML) and know-your-customer (KYC) rules often require linking transactions to your identity. Always stay informed about your local laws and reporting obligations when using cryptocurrency.

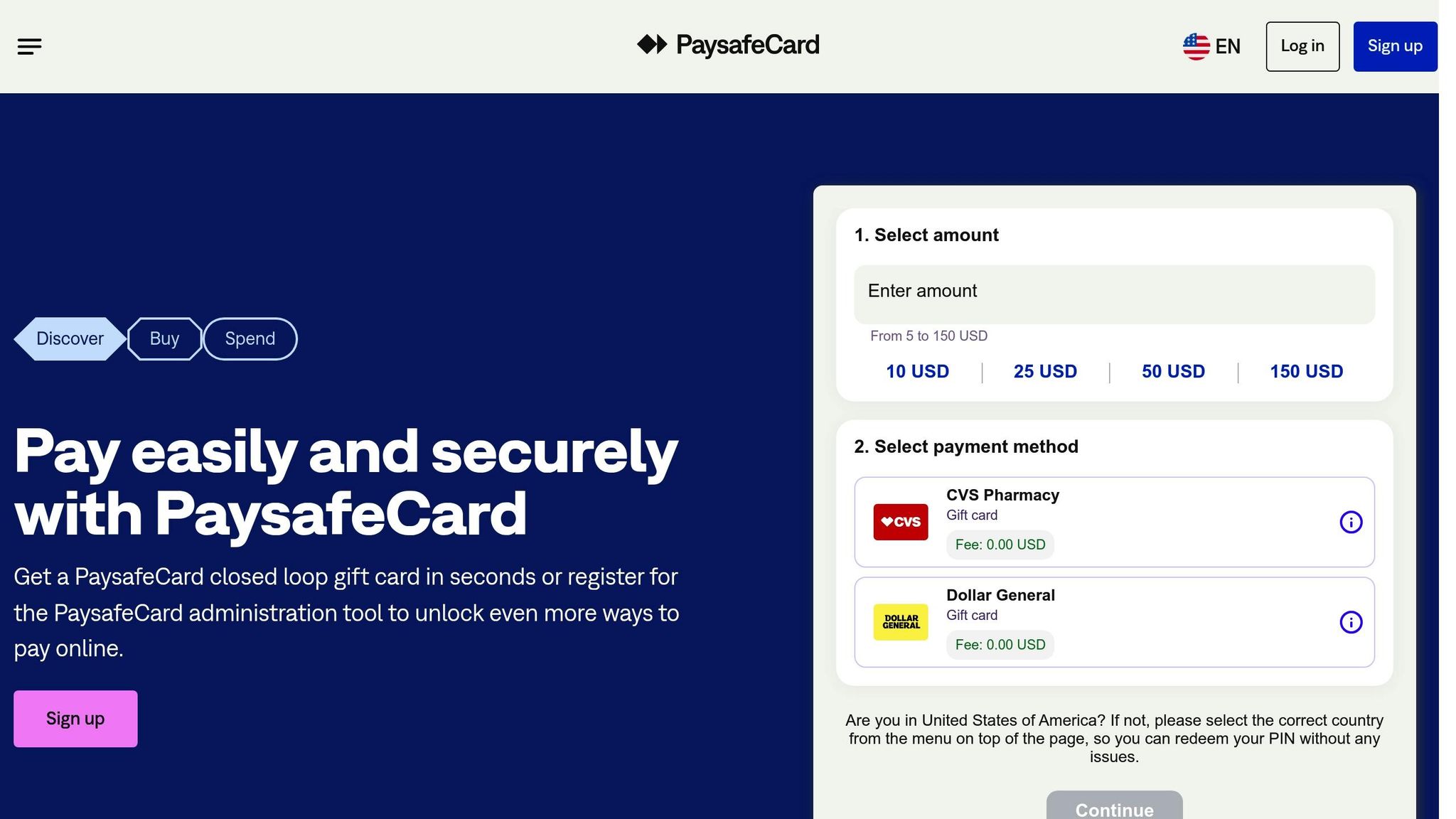

2. Paysafecard

Paysafecard is a prepaid voucher system that uses a unique 16-digit PIN as your payment method. It allows you to make purchases without providing any personal information.

Privacy Level: Full Anonymity vs. Semi-Anonymous

Paysafecard offers full anonymity when you buy vouchers with cash at physical retail locations. However, if you purchase a voucher using a credit card or another traceable payment method, your anonymity is compromised at the point of purchase . This balance between privacy and convenience makes it a popular choice for those who prioritize discretion.

Ease of Use and Accessibility

Paysafecard is designed to be straightforward. You can find vouchers at many retailers across the U.S. in denominations of $10, $25, $50, and $100. For larger purchases, you can combine up to 10 PINs in a single transaction . While registration is optional and unlocks additional features, it does reduce your level of anonymity. It’s worth noting that if you lose a PIN, you lose access to the funds associated with it.

Merchant Acceptance and Use Cases

Paysafecard is widely accepted by online merchants, including digital services, gaming platforms, and subscription-based websites. This makes it a great option for keeping your financial details private when shopping online. However, it’s primarily designed for online use, so you’ll need to confirm that a merchant accepts Paysafecard before completing a transaction. Physical stores typically do not accept these vouchers.

Geographic Availability

In the U.S., Paysafecard vouchers are available at numerous retail and online outlets, making them an accessible option for those seeking an anonymous way to pay online. Availability may vary by region, so it’s a good idea to check which local retailers carry them.

3. Cash App

Cash App is a mobile payment service available in the U.S. and the U.K. that uses a unique identifier called a $Cashtag instead of requiring your real name for transactions.

Privacy Level: Semi-Anonymous

Cash App provides a semi-anonymous experience by showing recipients only your $Cashtag, keeping details like your email, bank information, and full name private. However, setting up an account requires personal details, including your name, ID, phone number, and banking information. To safeguard your data, the platform encrypts payment history and bank account details, although it still links your $Cashtag to your real identity. Using false information during registration can lead to account suspension or failed transactions. You can tweak privacy settings to hide your name in transactions, but this comes with reduced limits for sending and receiving money compared to fully verified accounts. This balance between privacy and traceability makes it both secure and user-friendly.

Ease of Use and Accessibility

Cash App’s simplicity is one of its standout features. After downloading the app and setting up your $Cashtag, you can immediately start transferring funds. The app’s intuitive design also supports using a Cash App debit card, which works anywhere Visa is accepted.

Merchant Acceptance and Use Cases

Cash App is perfect for everyday transactions like sending money to friends or family. All the recipient needs is your $Cashtag to complete the transfer. You can also use it for purchases with merchants that accept Cash App. Additionally, the Cash App debit card extends this semi-anonymity to physical stores. When you use it at any Visa-accepting location, the transaction is recorded without exposing your personal information.

Geographic Availability

Currently, Cash App operates only in the U.S. and the U.K. In the U.S., its debit card can be used at any merchant that accepts Visa.

4. Virtual and Masked Credit Cards

Virtual and masked credit cards are a smart way to shield your real card details when making purchases. These services generate a unique, temporary number for each transaction, ensuring your actual card information stays hidden. If a website suffers a data breach, the compromised number becomes useless for future transactions.

Privacy Level: Semi-Anonymous

While virtual cards offer a layer of privacy, they don’t provide full anonymity. They protect your card details from merchants, but your card issuer and financial institution still track your transactions. Services like Google Wallet and Apple Pay use tokenization to enhance security. Google generates temporary numbers, while Apple uses device-specific tokens, ensuring merchants never see your actual card details or name.

However, it’s important to note that the payment processor collects data tied to your Google or Apple account, such as email or billing information. Google shares transaction details linked to your account, and Apple requires significant personal information during setup. This makes virtual cards great for maintaining privacy from merchants, though the platform itself will still have access to your identity.

Ease of Use and Accessibility

Setting up virtual cards is simple and quick. For example, Privacy.com offers browser extensions that let you create disposable virtual cards instantly. All you need is a linked bank account or debit card to get started.

Google Wallet works with any store that has Near-Field Communication (NFC) devices and is compatible with most websites. Similarly, Apple Pay provides convenience across multiple devices for both in-store and online purchases. Google Pay integrates seamlessly with other Google services, allowing you to send or request money directly through Gmail or Android messages. These features make virtual cards increasingly popular and easy to use.

Merchant Acceptance and Use Cases

Virtual cards are especially useful for online shopping, particularly when buying from less-trusted or unfamiliar websites. If a virtual card number is exposed in a data breach, it cannot be used to access your primary account.

Google Wallet and Apple Pay enjoy broad acceptance at retailers that support contactless payments. These systems rely on tokenization, which transmits a unique virtual account number instead of your actual credit card details during a transaction. This adds a significant layer of security, making it nearly impossible for intercepted transaction codes to be misused.

Privacy.com adds extra features like spending controls and card masking for enhanced security. For instance, you can set spending limits on each card or close them immediately after a purchase. Privacy.com even offers a free domestic plan for basic use.

That said, virtual cards aren’t universally accepted. Some older or smaller retailers may not support these payment methods, and they may not work with all online merchants, subscription services, or international transactions. For guaranteed acceptance, traditional payment methods remain the safer choice.

Geographic Availability

Virtual card services like Google Wallet, Apple Pay, and Privacy.com are widely accessible across the United States. Privacy.com offers a free domestic plan specifically for U.S. users. Google Wallet and Apple Pay function at most U.S. retailers with NFC-enabled payment terminals, which now include the majority of major stores and chains nationwide.

sbb-itb-e1a0769

5. Prepaid Gift Cards

Prepaid gift cards are a straightforward way to make anonymous payments. These cards, available in both physical and digital formats, can be purchased with cash at various retail locations like supermarkets, convenience stores, and big-box retailers. Since they don’t require ID verification, they’re a go-to option for maintaining privacy.

Privacy Level: Full Anonymity

When bought with cash, prepaid gift cards provide complete anonymity. You don’t need to share personal details, link a bank account, or use a credit card. However, while the purchase itself is private, any online transactions made with the card could potentially be tracked.

Ease of Use and Accessibility

Using prepaid gift cards is as simple as it gets. After buying one with cash, you’ll use the card number, expiration date, and security code at checkout for online purchases. They’re widely available across the U.S., found in grocery stores, pharmacies, and retail chains. With denominations typically ranging from $10 to $100, they’re accessible and convenient for quick, anonymous transactions.

Merchant Acceptance and Use Cases

These cards are often retailer-specific. For example, an Amazon gift card can only be used on Amazon, while a Steam card works exclusively on Steam. They’re ideal for one-time purchases like ebooks, apps, or other digital content. If you need to make a larger purchase, many retailers allow you to combine multiple gift cards during checkout. However, prepaid gift cards aren’t suited for recurring payments, bills, or purchases across multiple merchants. Additionally, losing the physical card means losing access to any remaining balance.

Geographic Availability

Prepaid gift cards are most commonly found in the United States, where major retailers have a widespread presence. You’ll find them in nearly every grocery store, pharmacy, and retail outlet. That said, these cards often come with geographic restrictions. For instance, an Amazon.com gift card bought in the U.S. might not work on Amazon’s international sites. To avoid issues, it’s best to use them within the country where they were purchased.

6. Prepaid Debit Cards

Prepaid debit cards offer a flexible and private way to handle payments, making them a step up from gift cards in terms of versatility. They function like regular debit cards but aren’t tied to any bank account. Instead, you load them with cash and use them anywhere Visa or Mastercard is accepted, all while keeping your identity under wraps.

Privacy Level: Full Anonymity

When purchased with cash and without providing an ID, these cards offer complete anonymity. There’s no Know Your Customer (KYC) verification involved, which means your personal details stay private. While card issuers might track spending patterns, they won’t link this activity back to your identity. This makes prepaid debit cards a more private option than linked payment methods like Cash App or traditional bank cards, though they’re still slightly less anonymous than using cash.

Ease of Use and Accessibility

Getting a prepaid debit card is refreshingly simple. You don’t need to fill out applications, go through credit checks, or provide any identity verification if you’re paying with cash. These cards are easy to find at popular retailers like Walmart, Target, CVS, Walgreens, and other supermarkets or convenience stores. Once you activate the card and load funds onto it, you can start using it right away, making it a hassle-free option.

Merchant Acceptance and Use Cases

One of the biggest advantages of prepaid debit cards is their broad acceptance. Cards branded with Visa or Mastercard are honored at millions of locations worldwide, from online stores to physical retailers. They’re great for online shopping, in-store payments, bill payments, and even ATM withdrawals. While some merchants may refuse prepaid cards due to fraud prevention policies, the vast majority accept them, making them a practical choice for protecting your main bank account information.

These cards are also useful for budgeting since you can load only what you plan to spend, helping you avoid overspending. Plus, if the card is ever lost or compromised, your potential loss is limited to the amount loaded. They’re particularly handy for one-time purchases or temporary spending needs when you want to keep your finances separate.

Geographic Availability

Prepaid debit cards are widely accessible across the United States, available at major retailers in most cities and towns. They’re also offered in many other developed countries, though the brands and options may vary by region. Some countries impose restrictions or require identification for purchases exceeding a certain amount. Most Visa and Mastercard prepaid cards can be used globally, wherever those networks are accepted. However, keep an eye out for fees, as some cards may charge inactivity fees if left unused for too long.

7. Cash and Cash-by-Mail

When it comes to anonymous payment methods, cash is the gold standard. Unlike digital options, cash transactions don’t require personal information, account setups, or leave any kind of digital trail. It’s as private as it gets.

When you pay with cash in person, there’s no exchange of personal or digital details. You hand over the money, receive your goods or services, and walk away – no data is collected, no accounts are linked. If privacy is your top priority, cash is the go-to option.

For online shopping, cash-by-mail offers a creative way to maintain this level of privacy. By sending physical currency through the mail, you can pay for goods without sharing a return address. While not as common today, some businesses still accept cash-by-mail for those who value privacy over speed. However, keep in mind that this method is slower and carries some risks, like lost or stolen payments.

Privacy Level: Full Anonymity

Cash offers unmatched privacy. You don’t need to share your name, credit card information, email address, or anything else that could identify you. The seller only receives the physical money, making it impossible to trace the transaction back to you.

Cash-by-mail extends this same level of anonymity to online purchases. You can pay without revealing your identity or location. That said, sending cash through the mail comes with risks. There’s no fraud protection, and if the money gets lost or stolen, you’re out of luck.

Ease of Use and Accessibility

Using cash in person is simple – no apps, no accounts, no tech skills needed. You just hand over the bills and you’re done. It’s accessible to everyone, regardless of financial history or technical know-how, and it doesn’t require credit checks or verification.

Cash also makes budgeting easier since you can physically see and manage your money. However, as more businesses shift to digital payments, cash is becoming less convenient. In urban areas, cash acceptance is declining, and online-only retailers rarely accept it. Access to ATMs and cash-friendly businesses is crucial for those who rely on physical currency.

Cash-by-mail adds another layer of complexity. While it allows for anonymous online purchases, delivery times are slower than digital payments, and there’s always the risk of loss or theft. Plus, not all businesses accept this method, limiting its usability for certain online transactions.

Merchant Acceptance and Use Cases

Cash is still widely accepted at most physical stores in the United States. Grocery stores, restaurants, gas stations, and small businesses generally welcome cash payments. It’s especially useful for everyday purchases, tipping, and dealing with vendors who don’t use digital payment systems.

Some specialized merchants, like farmers markets, street vendors, and informal service providers, often prefer cash to avoid digital records. However, in urban areas, the trend toward cashless payments is growing, while rural and suburban regions tend to stick with cash-friendly practices.

That said, relying solely on cash in 2026 could be tricky. It’s not practical for online services like streaming subscriptions or digital products. For these situations, you’ll need to pair cash with other anonymous payment methods.

Geographic Availability

Cash is legal tender across the United States and is easily accessible through ATMs nationwide. However, some financial institutions have scaled back their ATM networks, especially in urban areas. In contrast, rural and suburban areas generally maintain stronger cash acceptance and infrastructure.

One important legal note: transactions over $10,000 in cash must be reported to the Financial Crimes Enforcement Network (FinCEN) under anti-money laundering laws. This primarily applies to businesses and financial institutions, not everyday consumers. Attempting to break up transactions to avoid these reports – known as “structuring” – is illegal. For typical personal purchases, though, cash remains a straightforward and unrestricted option.

In short, cash offers unparalleled privacy and is free from data breaches since no digital information is involved. For in-person transactions where anonymity matters, cash is unbeatable. However, for online purchases and digital services, you’ll need to combine it with other private payment methods to navigate today’s increasingly digital landscape.

Comparison Table

Here’s a quick breakdown of key features for each payment method to help you weigh your options effectively:

| Payment Method | Privacy Level | Ease of Use | Geographic Availability | Merchant Acceptance | Setup Requirements | Best For |

|---|---|---|---|---|---|---|

| Cryptocurrency | High (if handled carefully) | Moderate | Global (with some restrictions) | Limited to tech-driven merchants | Wallet setup and exchange account | Tech-savvy users making international transfers |

| Paysafecard | Complete (when purchased with cash) | Easy | Available in many countries through retail vendors | Numerous online retailers and some physical locations | Purchase voucher at retail – no registration needed | Online shopping with complete anonymity |

| Cash App | Partial | Very Easy | US and UK only | Peer-to-peer and some online merchants | Account required (with a $Cashtag alias) | Peer-to-peer transfers between friends in the US |

| Virtual and Masked Credit Cards | Partial | Easy | US and most developed nations | Anywhere Visa or Mastercard is accepted | Existing credit card account | One-time online purchases from unfamiliar merchants |

| Prepaid Gift Cards | Partial | Very Easy | US and most developed nations | Merchants accepting the specific card brand | Purchase and activation only | Casual online shopping |

| Prepaid Debit Cards | Partial | Very Easy | US and most developed nations | Merchants accepting the specific card brand | Purchase and activation only | Staying “under the radar” with limited funds |

| Cash and Cash-by-Mail | Complete | Very Easy (in-person) / Complex (by-mail) | Universal | Universal in physical stores / Limited online | None | In-person purchases where complete anonymity is essential |

This table highlights the balance between privacy and convenience for each method. Limits differ widely: Paysafecard lets you combine up to 10 PINs, cash is only limited by what you carry, prepaid and virtual cards depend on loaded amounts or credit limits, Cash App has lower limits without verification, and cryptocurrency limits vary by exchange policies. Costs also vary – cash is fee-free, while prepaid cards may have activation or maintenance fees, Cash App charges instant transfer fees, and cryptocurrency involves exchange fees. Lastly, security varies: cash is immune to cyber risks, virtual cards generate unique numbers for each transaction, Paysafecard requires no personal data, and cryptocurrency security hinges on proper wallet management.

Conclusion

Picking the best anonymous payment method in 2026 comes down to what matters most to you – absolute privacy, digital convenience, or a mix of the two. Here’s a quick breakdown of the trade-offs for each option.

If you’re looking for in-person privacy, cash and cash-by-mail remain the top choices for keeping transactions completely off the grid. For online purchases, Paysafecard offers strong anonymity, especially when bought with cash. Privacy-focused cryptocurrencies like Monero and Zcash also provide solid anonymity for digital transactions, though they require a bit of technical know-how.

For those who prioritize ease of use but still want some level of privacy, virtual and masked credit cards are widely accepted anywhere Visa or Mastercard is used. If you’re in the U.S., Cash App offers fast peer-to-peer transfers using a unique $Cashtag, though it trades off some anonymity for convenience.

Prepaid gift cards and debit cards strike a balance between privacy and practicality. They’re easy to set up, cost-effective, and work well for both online and in-store purchases. However, they often come with spending limits and may not be ideal for recurring payments.

In summary, every method involves a trade-off between privacy, convenience, and compliance with regulations. Many digital payment providers collect personal data due to anti-money laundering and know-your-customer laws.

To choose the right option, align your payment method with your transaction needs. Use Paysafecard or cash for maximum anonymity, virtual credit cards for protecting your payment details with unfamiliar merchants, Cash App for quick peer-to-peer transfers, and prepaid cards for everyday purchases where staying discreet is a priority. By weighing these options, you can find the best fit for your privacy and convenience needs in 2026.

FAQs

What are the best practices for staying anonymous when using cryptocurrencies for transactions?

When prioritizing anonymity in cryptocurrency transactions, it’s wise to opt for privacy-focused coins such as Monero or Zcash. These coins come with built-in features specifically designed to keep transaction details private. On the other hand, steer clear of wallets or exchanges that require identity verification (KYC) since linking your personal information to your transactions compromises your privacy.

Another step to consider is using a VPN to hide your IP address when accessing cryptocurrency platforms. This simple measure can shield your online activity and provide an extra layer of protection. For in-depth reviews on VPNs that emphasize security and privacy, resources like those from Cloud Explorer can be incredibly helpful.

What are the risks and downsides of using cash-by-mail for online purchases?

Using cash-by-mail for online shopping carries quite a few risks and drawbacks. For starters, cash can get lost, stolen, or even damaged during shipping, and once it’s gone, it’s nearly impossible to recover. Unlike digital payment methods, this approach doesn’t offer any buyer protection, leaving you exposed if the seller doesn’t follow through on their end of the deal.

On top of that, sending cash through the mail can be slow and unreliable, especially over long distances. It’s also not a secure or commonly accepted method for most online purchases, which can seriously limit your options. If you’re looking for safer ways to pay, consider alternatives like cryptocurrencies or prepaid cards, which offer more security and flexibility for anonymous transactions.

What makes prepaid debit cards more private than traditional debit cards?

Prepaid debit cards provide a layer of privacy that traditional debit cards simply can’t match. Since they’re not tied directly to your bank account, your personal financial details stay shielded during transactions. This added separation helps reduce the risk of exposing sensitive banking information. Plus, many prepaid cards can be bought with cash, allowing for an anonymous purchase – perfect for those who value extra discretion.

That said, it’s important to note that some prepaid cards might require you to register or provide identification to activate them. Be sure to check the terms and conditions before making a purchase to ensure the card aligns with your privacy preferences.